The international debt crisis and the problem of all Mexicans

If you enjoy our content, we invite you to support our work by subscribing to our premium news service. Your subscription will allow us to continue with our work and will also give you access to exclusive content. We appreciate your support in advance!

The world has become addicted to debt in order to grow, and that is something that should concern us all. The indebtedness of governments, corporations, banks and households increases month by month, reaching levels never seen before. Government liabilities alone are equivalent to the size of the world’s Gross Domestic Product (GDP), which will have a high cost for their populations.

The debt burden has grown so much due to the current context of high interest rates that it now represents a growing threat to living standards in all economies.

The problem is that most politicians prefer to ignore the problem and are not willing to speak frankly about the urgent need to improve tax collection and be more efficient with public spending. Instead, they make wasteful promises that, at the very least, increase inflationary pressures.

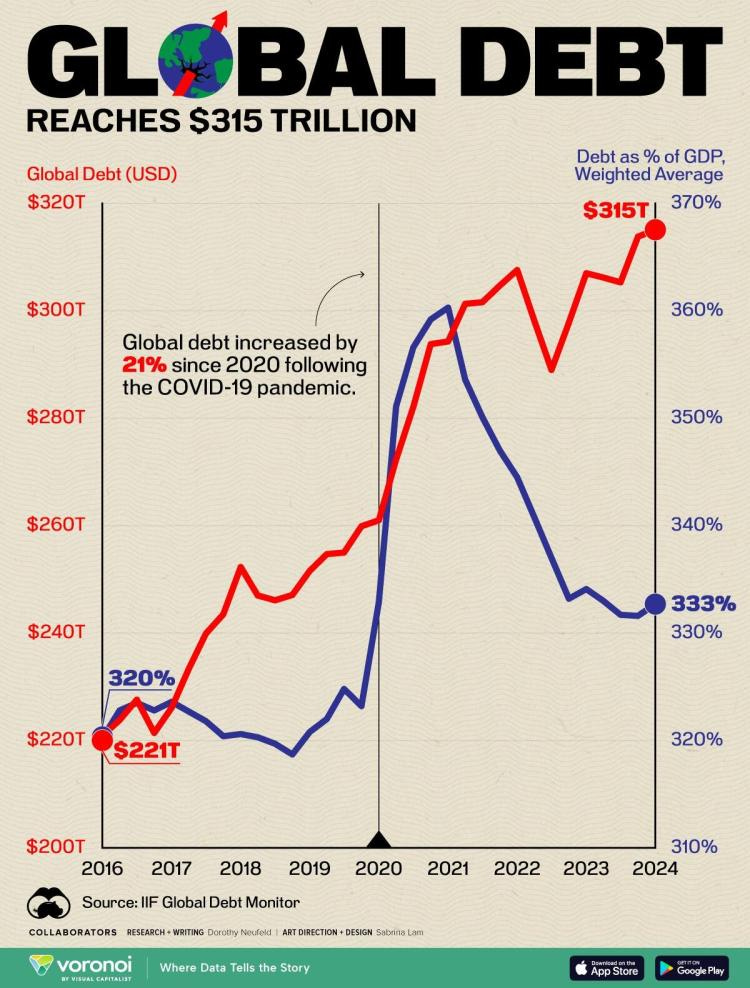

In this regard, an article published on the Zerohedge portal on August 16 and titled “Global debt hits a new high of $315 trillion” reports that the volume of global debt reached a new record in the first quarter of 2024, increasing by an additional $1.3 trillion in just three months.

This avalanche of borrowing is a broad trend across all economies.

While the United States and Japan were the largest contributors in advanced economies, China, India, and Mexico drove the largest debt growth in emerging markets.

Overall, the total global debt-to-GDP ratio reached 333% as higher interest rates translate into high debt service costs, causing rising debt burdens to continue to pile up.

The chart below, by Dorothy Neufeld of Visual Capitalist, shows the global debt stock in 2024, based on data from the Institute of International Finance (IIF).

Since the start of the Covid-19 pandemic in March 2020, debt has increased by 21%, adding $54.1 trillion to the global total.

Today, the bulk of debt is held by non-financial corporations, at $94.1 trillion, while government borrowing follows closely behind at $91.4 trillion. Meanwhile, the financial sector is saddled with $70.4 trillion in debt and households are saddled with $59.1 trillion.

While stimulus measures during the pandemic did prompt more borrowing at the time, they are now leaving many economies in a more precarious situation. We know that there was no government support in Mexico during the pandemic, but that does not mean that debt has not stopped growing, as I have discussed in previous posts. In the United States, meanwhile, debt service costs are now higher than defense spending, and the interest bill will rise even further. In Mexico, it is estimated that this year the interest payments on the debt will total 1.2 trillion pesos, which represents 3.3% of the Gross Domestic Product (GDP) and 16.5% of the federal government’s budget revenues.

As a result, governments now need to raise taxes or cut spending to address their growing debt burden. So far, no political party has a meaningful strategy to address the country’s fiscal sustainability in the medium and long term.

For emerging markets, such as Mexico, rising debt burdens pose greater risks. These risks are especially acute given that the country will experience lower economic growth in a high-interest rate environment, which is expected to occur by 2025.

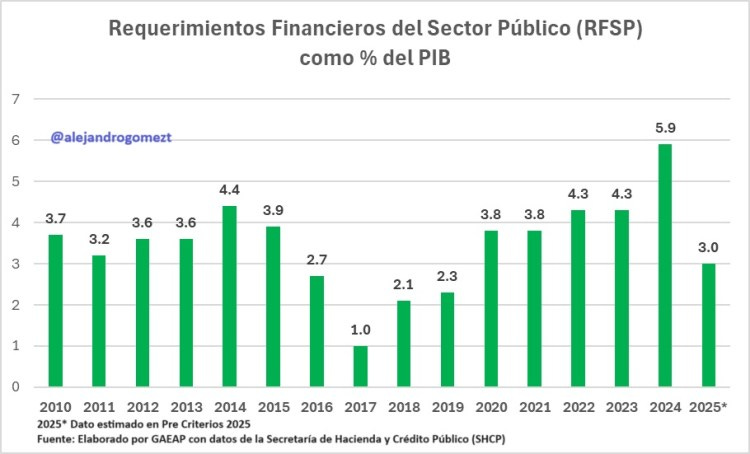

The Mexican public deficit increased by 51% at the end of the first half of the year

As expected, according to data from the Ministry of Finance and Public Credit (SHCP), the fiscal deficit, measured through the Public Sector Financial Requirements (PSFR), showed double-digit annual growth in the first half of the year, in addition to being at its highest level since records began.

Between January and June 2024, the PSFR stood at 821 billion pesos (mmdp), which represented a growth of 51.2% compared to the 543 billion pesos recorded in the same period last year.

As I have mentioned in this space, it is expected that this year the PSFR will be at a level not seen since the 1980s. The Treasury’s projections show that, at the end of this year, they would be at 5.9% of GDP, due to greater indebtedness during an election year and to finish the flagship projects of the current administration, such as the Mayan Train and the Dos Bocas Refinery.

Thus, the debt ceiling approved by the Congress of the Union is 1.9 trillion pesos in the domestic market, while for external debt the authorized amount was 18 billion dollars.

Meanwhile, for 2025, the first year of Claudia Sheinbaum’s administration, the SHCP expects the deficit to decrease to 3% of GDP, something that seems practically impossible without a fiscal reform, a point that I will address later in this installment.

It is worth remembering that according to figures from the Treasury, last June the Historical Balance of the PSFR (the broadest measure of debt) reached an amount of 16.030 trillion pesos, a figure equivalent to 47.8% of GDP (assuming that the nominal GDP, which has not yet been published, is 33.54 trillion pesos).

The figures confirm that although the official discourse of President López Obrador and the officials of the Treasury Department is to the effect that the current administration has not indebted the country, the data say otherwise. In 2024, the (expanded) public debt as a percentage of GDP is at its highest level since 2000. And the only reason why the debt did not rise more as a percentage of GDP is because there was high inflation and meager economic growth. Here is an example:

If the nominal GDP is 33.54 trillion pesos and the debt is 16.03 trillion pesos, this means that the weight of the debt in relation to the GDP is 47.8%, as mentioned above. If after one year the GDP deflator (inflation) is 5% and the annual economic growth is 2%, this means that the following year the nominal GDP will be 35.92 trillion pesos. If in that same period the fiscal deficit is 3.5% of the GDP, this implies an additional debt of 1.25 trillion pesos, which would bring the debt balance to 17.28 trillion pesos and the debt weight to GDP ratio to 48.12%. In this way, it is clear that inflation helps the government to borrow significantly without raising the debt to GDP ratio too much.

The fiscal deficit target for 2025 is unattainable

The Ministry of Finance expects that in 2025 the public deficit will be reduced to less than half of that observed this year, which they plan to achieve through fiscal consolidation and spending cuts, without implementing a tax reform.

In this sense, analysts find it difficult that, only with spending cuts, the financial requirements can reach a level of 3% or even 3.5% of GDP next year. In this sense, it should be noted that in the Pre-Economic Policy Criteria 2025, the SHCP mentions that the PSFR would be 3.0%, while in some speeches, the president-elect Claudia Sheinbaum has mentioned the figures of 3.0% and 3.5% of GDP in the PSFR.

A few days ago, the Center for Economic and Budgetary Research (CIEP) published a study in which it pointed out that the cuts to public spending that have been mentioned so far, as well as a lower interest rate, will not be sufficient to reach 3% of GDP, so a tax reform will be needed to broaden the taxpayer base.

CIEP calculations showed that the completion of the flagship works, as well as a reduction in average interest rates, could reduce the public deficit by 1.1% of GDP, and while this could be combined with an increase in revenue of 0.8% of GDP due to a fight against informality and greater revenue from import taxes, as well as lower financial costs, it would not be enough to reduce the deficit to 3% of GDP in 2025.

According to CIEP, this year’s Federal Expenditure Budget (PEF) implies that total spending will reach a level of 26.7% of GDP, equivalent to about 9 trillion pesos. Of this amount, 63.3% of this expenditure is unavoidable commitments, which include the financial cost of the debt (3.3% of GDP), the expenses of Petróleos Mexicanos (Pemex) and the Federal Electricity Commission (CFE) (3.7%), contributions to the federal entities (4.0%) and pensions (5.9 percent).

The remaining amount, which is 26.6% of the GDP, is non-unavoidable expenses. Of this total, 3.3% of the GDP is allocated to education, 2.9% of the GDP to health, 1.7% to investments, and 2.0% to other expenses.

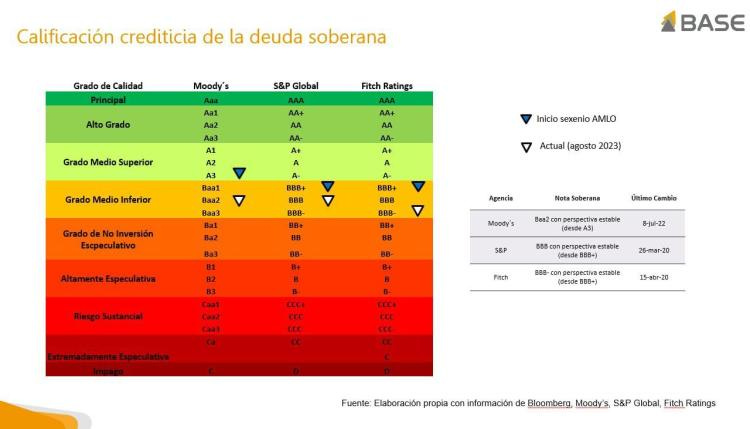

It is in this complicated context of chronic fiscal deficit, high inflation and lower economic growth that Mexico runs a real risk of having its sovereign debt rating downgraded. If this scenario materializes, it would lead to an increase in interest rates and a greater depreciation of the peso against the dollar.

Tax reform is necessary

Thus, in order for the next government to be able to reduce the fiscal deficit, it is necessary to make the criteria for allocating uncommitted public spending more efficient. Likewise, a comprehensive tax reform is necessary to increase the taxpayer base and increase public revenues to face the pressures and needs of greater public spending. Something fundamental is to consider fiscal equity, with fair burdens and benefits among all social sectors and between present and future generations.

Regrettably, the current federal administration refused to carry out a tax reform and, instead, implemented a series of Tax Miscellanies to combat tax evasion by eliminating universal compensation, in addition to launching an aggressive audit of large taxpayers.

Meanwhile, Claudia Sheinbaum has also expressed herself against implementing a tax reform, at least at the beginning of her six-year term, despite the recommendations that have been made on the matter. The issue is delicate and few are analyzing it with the seriousness that should be.

These are times of great uncertainty and we need to be informed. Listen us on ECONOMEX Podcast Episode 20 here: